In today’s world, Kazakhstan carries out significant improvement work for the economic situation of the country. As part of a commission from Head of State, National Bank of Kazakhstan has revoked licenses of three commercial bank pursued high-risk policy (NBK, 2017). Furthermore, over the past 10 years, 7 second-tier banks have gone into liquidation as well as the liabilities of the commercial banks as a whole have increased by 70 per cent or 5.5 trillion Tenge (Hereinafter — KZT). NBK plans to continue treatment the real economy sector, withdrawal of financial institution, restructuring its assets to well-balanced entities.

On the other side of the world, the digital and mobile banks namely, Starling bank, Monzo, N26 are becoming increasingly popular among society in the United Kingdom. As a vivid illustration, Starling Bank has increased considerably the number of customers for 8 times (up to 400 000 people) at the end of the 2018 year (Starling Bank, 2019). At the same time, one million clients have joined and used Monzo’s services (Monzo). Such tendency establishes substantial competition for all players including high-street banks in the payments market.

In consequences, the main object of the paper is identification the advantages of digital bank and illumination capabilities to deploy analogous mobile bank in Kazakhstani real financial sector.

The raising awareness of digital banks has corresponded with the period of implementation of the measure as Payment Services Directive 2 (PSD2) for reducing encumbrances international payments among European Union countries and provides a foundation for innovative online payment (Eur- lex, 2017, cited in Thorell, J. and Sjostrand, J., 2017). Although, the non-minor reasons for the deployment of PSD2 were the regulation and catching threats against financial frauds (Computer Fraud & Security, 2017).

Additionally, Open Banking programme issued in Open Banking Standards (OBS) by the Competition and Market Authority (CMA) also weighted in digital bank’s favour (Haslingden, 2018). The system is based on the usage of application programming interfaces (API) approving companies without obstruction and reliable distributes data of transitions and current accounts (ibid). API technology is used on the Uber platform, where taxi location and customer request visually represented on a map (Uber.com).

As for Starling API, it doesn’t only combine the services for improving the quality of customer satisfaction, and deployment the Marketplace where clients have a right to choose alternative party products such as insurance, mortgage and loans (Starling Bank). All necessary financial services are

jointed and demonstrated on APIs platform. The documentation and developer infrastructure of Starling APIs are open sourced and everyone is able to handle for combining extra and independent application by a third entity (ibid). In particular, it is allowed to launch Bank-as-a-Service (BaaS) as new paradigm, besides of basic paradigm of IT services namely, software as a service (SaaS), infrastructure as a service (IaaS), and platform as a service (PaaS) (J. Park, Y. An and K. Yeom, 2015).

Moreover, Starling bank takes preference over the traditional bank by comparing the provided financial instruments and services. Starling Bank asserts that there is no fee for a personal account and joint current account where usual bank includes an additional commission on its financial goods (Starling Bank). It provides one specific user account for using the range of third-party products placed on Marketplace; consequently, every fee and commissions lay down on partners (ibid). On top of it, the mobile-only bank focuses on taking a percentage of interchange transaction income from an entity that provides product or service than from customers. Additionally, Bank claims that all ATMs located in the UK don’t request a commission for withdrawing Sterling while HSBC charges from its client a 2.75% and other typical banks charge approximately the same fee (ibid). As well as there is free withdraw in outside the UK and no charge for payments in foreign currency by Starling Bank.

This report is theoretical research starting with searching literature in the library associated with “digital and open bank”. After selecting the essential articles, data the work is done according to the capacity of realization of a mobile bank based on API framework and reliable innovative technologies. The result can be helpful in Kazakhstan for investment and development of the country.

At the moment Kazakhstan has already experience of implementation, becoming the first electronic public framework launched in Central Asia (Kaulanova A., 2017). It is one the initial public system is deployed by API in keeping with Electronic Government as a Service (EgaaS). This has enabled to process just over 40 million electronic requests annually and the number registered users gained on 6 million in 2017 (Egov.kz, 2017). According to the Global UN’s e-Government Knowledgebase (2018), Kazakhstan takes the 39th position of 193 countries.

Going to the bank sector, the situation is slightly different. It is by looking at the information provided by Forbes.kz, the 10 largest commercial banks of Kazakhstan have a stable position (Vorotilov, A. and Aulbekova, A., 2018). There are Halyk Bank JSC, Kaspi Bank JSC, Housing Construction Saving Bank of Kazakhstan JSC, Tsesnabank JSC, SB Sberbank of Russia JSC (Hereinafter — Sberbank), Bank CenterCredit JSC, ForteBank JSC, SB Home Credit Bank JSC, Altyn Bank JSC and ATF Bank JSC (ibid). Most of these banks have own internet version of banking., except Tsesnabank acquired by First Heartland Bank JSC hasn’t mobile and web bank, the online banking work is in progress (First Heartland Bank, 2019).

For instance, the largest bank of Kazakhstan, Halyk Bank after merging with Kazkommertbank that holds 40% market share has myHalyk integrated with Homebank, which the previous owner is Kazkommertbank (Foy, H., 2017). MyHalyk is able to show user’s loans, payment cards and provides money transfer between accounts and others, payment services, account statement as well as currency conversation between Tenge and major currencies (MyHalyk).

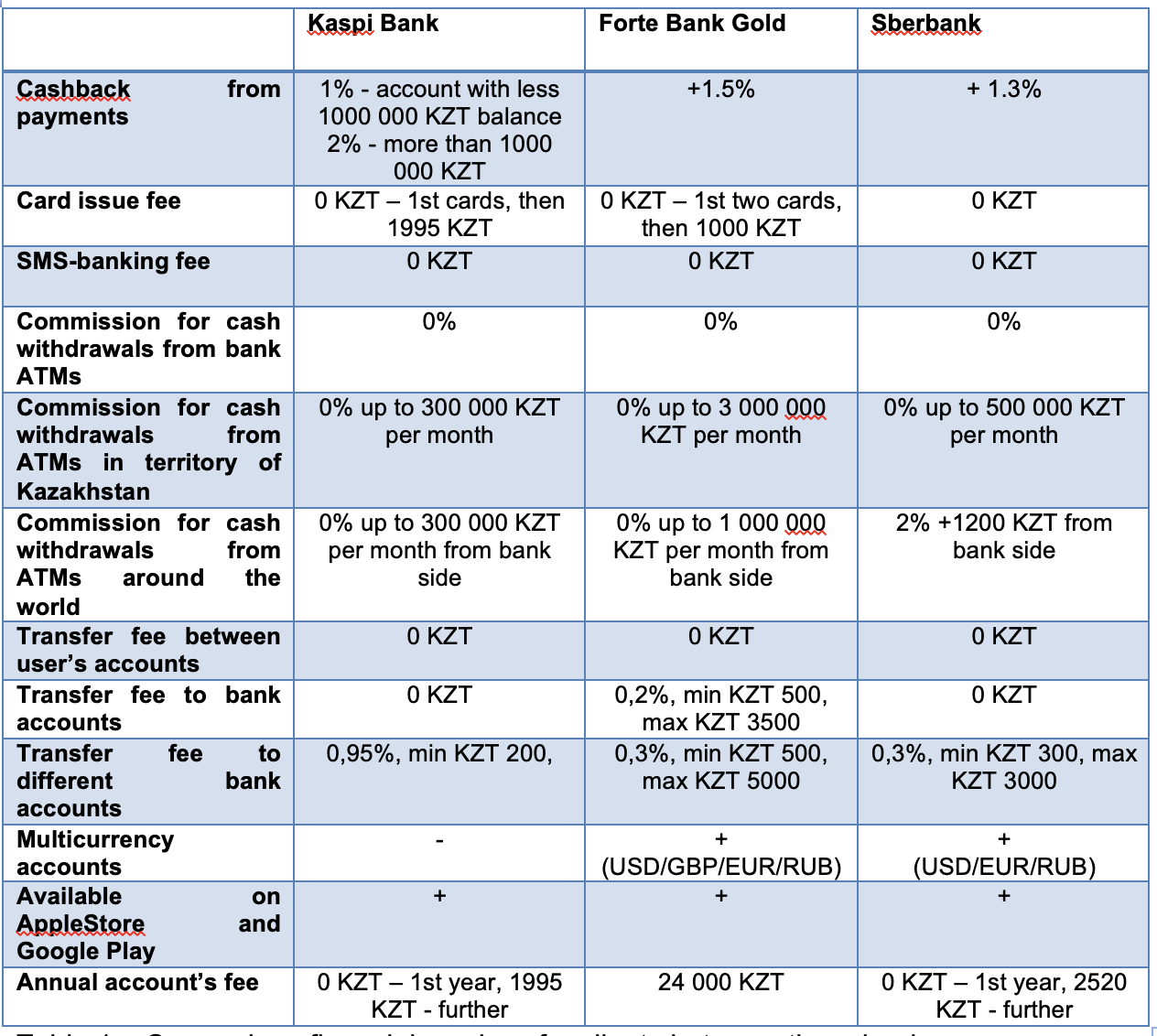

However, Kaspi Bank, ForteBank and SberBank provide to society one of the attractive online bank services and their main offers are demonstrated in table1 (Kaspi Bank; ForteBank; SberBank).

Table 1 – Comparison of financial services for clients between three banks.

For security and rapid payments Sberbank, as well as ForteBank, have launched online purchase by ApplePay (Sberbank; ForteBank). At the same time, Kaspi Bank offers to clients instalment purchase of a large number of goods without any extra cost and commission among partner stores of the bank (Kaspi Bank).

Unfortunately, none of the financial institutions of Kazakhstan hasn’t launched the Open API platform allowing to establish interaction between applications for third party companies. This issue provides opportunities for launching digital and mobile bank on the territory of Kazakhstan.

Requirements and opportunities for implementation of a mobile bank

In the previous chapters, the advantages of Starling Bank, as well as the situation of web and mobile banking in Kazakhstan, are discussed. The customer policies of most commercial banks have attractive conditions for clients.

Going to requirements that newly created commercial bank meets to be licensed, the financial regulations are reviewed. According to “On banks and bank activities” Act of the Republic of Kazakhstan, all licensed banks providing financial services are a mandatory member of the insurance system (KDIF, 2019). Due to the fact, the client deposit operated into account is recovered by Kazakhstan Deposit Insurance Fund any terms and conditions (ibid).

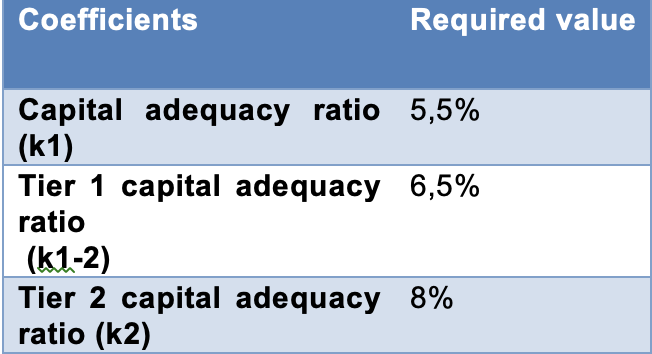

Moreover, considering establishing regulatory and calculation methodology for prudential regulation and other mandatory to the observance of the norms and limit of bank capital on given data and Rules of calculation and limits of open foreign exchange position was approved by a Decision of the Board of the National Bank of the Republic of Kazakhstan dated by 13 September 2017 (NBK, 2017). In the document is posted that the minimum- net worth for commercial bank is required to 10 billion KZT(ibid).

Secondly, the following coefficients illustrated in table 2 are entered for determining the capital adequacy of the bank:

Table 2 – The value of capital adequacy ratio (NBK, 2017)

NBK claims that assets, contingent and unforeseen liabilities weighted by risk ratio and introduced in the k1, k1-2, k2 coefficients are formed according to International Financial Reporting Standard (FRS) (NBK, 2017). Besides, the Board’s Decision consists of supplementary and vital requirements for commercial banks such as capital adequacy ratio based on conversation buffer and a mandatory buffer which are not included in the report (ibid).

Another point that should be mentioned, related to human resources of professional IT staff which possible maintains and develops a digital financial product with using last innovative technologies. Kireyeva, A. A., Mussabalina, D. S. and Tolysbaev (2018) believe that in general the IT development of Kazakhstan has acceptable performances where Almaty and Astana play a significant role. The main reasons are educational power of contemporary education institutions as Nazarbayev University works at the same level as western universities or International IT-University collaborated with University Carnegie — Mellon (ibid). In addition, Kazakh-British Technical University trains students in different academic programs who regularly participate in the Association for Computing Machinery – International Collegiate Programming Contest (ACM ICPC) World Championship (KBTU, 2019). As well as KBTU is able to prepare high-level educated students within a double diploma with the London School of Economics for the financial sector (QS Top Universities, 2019). It is an excellent performance of quality education accredited by institution namely IMarEST and Computer Accreditation Commission of ABET and cooperation with British universities (ibid).

Thirdly, in a place where the event of the international specialized exhibition EXPO-2017 was located, the government organized the Astana startup Hub for establishing an innovative project and IT ecosystem (Astana Hub). At the moment, 189 startups, 2034 participants and 60 investors have registered in Astana Hub, the Framework is planning to attract 67 billion KZT as an investment by 2022 (ibid). One of the benefits for launching IT-products within Hub is Law of the preferential tax regime for Astana Hub participants signed by President of the Republic of Kazakhstan (Astana Hub). The document envisages the incentives on a corporate tax income, on individual income tax, on value-added tax, on profit including non-resident and dividends (ibid).

The aim of the essay is to demonstrate the capabilities of the launching digital and mobile bank as Starling Bank uses the innovate approach as an Open API platform (Starling Bank). It was outlined an absence of implementation web bank based on Open API system in Kazakhstan and market situation of domestic high-street banks licensed by National Bank of Kazakhstan which provide financial services. Its services were compared in detail. On the other hand, it was underlined the path where possible to recruit graduated students from Nazarbayev University, International IT-University, (Kireyeva, A. A., et. al., 2018) and Kazak-British Technical University as well- educated engineers to maintain new technologies of the project and professionals in finance and management for the regulation business process (QS Top Universities., 2019). Moreover, it was able to skate the various types of financial preferences of registered residents in Astana Hub who launch products as new high-tech startups (Astana Hub).

On the other side of the world, the digital and mobile banks namely, Starling bank, Monzo, N26 are becoming increasingly popular among society in the United Kingdom. As a vivid illustration, Starling Bank has increased considerably the number of customers for 8 times (up to 400 000 people) at the end of the 2018 year (Starling Bank, 2019). At the same time, one million clients have joined and used Monzo’s services (Monzo). Such tendency establishes substantial competition for all players including high-street banks in the payments market.

In consequences, the main object of the paper is identification the advantages of digital bank and illumination capabilities to deploy analogous mobile bank in Kazakhstani real financial sector.

Background

The raising awareness of digital banks has corresponded with the period of implementation of the measure as Payment Services Directive 2 (PSD2) for reducing encumbrances international payments among European Union countries and provides a foundation for innovative online payment (Eur- lex, 2017, cited in Thorell, J. and Sjostrand, J., 2017). Although, the non-minor reasons for the deployment of PSD2 were the regulation and catching threats against financial frauds (Computer Fraud & Security, 2017).

Additionally, Open Banking programme issued in Open Banking Standards (OBS) by the Competition and Market Authority (CMA) also weighted in digital bank’s favour (Haslingden, 2018). The system is based on the usage of application programming interfaces (API) approving companies without obstruction and reliable distributes data of transitions and current accounts (ibid). API technology is used on the Uber platform, where taxi location and customer request visually represented on a map (Uber.com).

As for Starling API, it doesn’t only combine the services for improving the quality of customer satisfaction, and deployment the Marketplace where clients have a right to choose alternative party products such as insurance, mortgage and loans (Starling Bank). All necessary financial services are

jointed and demonstrated on APIs platform. The documentation and developer infrastructure of Starling APIs are open sourced and everyone is able to handle for combining extra and independent application by a third entity (ibid). In particular, it is allowed to launch Bank-as-a-Service (BaaS) as new paradigm, besides of basic paradigm of IT services namely, software as a service (SaaS), infrastructure as a service (IaaS), and platform as a service (PaaS) (J. Park, Y. An and K. Yeom, 2015).

Moreover, Starling bank takes preference over the traditional bank by comparing the provided financial instruments and services. Starling Bank asserts that there is no fee for a personal account and joint current account where usual bank includes an additional commission on its financial goods (Starling Bank). It provides one specific user account for using the range of third-party products placed on Marketplace; consequently, every fee and commissions lay down on partners (ibid). On top of it, the mobile-only bank focuses on taking a percentage of interchange transaction income from an entity that provides product or service than from customers. Additionally, Bank claims that all ATMs located in the UK don’t request a commission for withdrawing Sterling while HSBC charges from its client a 2.75% and other typical banks charge approximately the same fee (ibid). As well as there is free withdraw in outside the UK and no charge for payments in foreign currency by Starling Bank.

The situation of banking systems in Kazakhstan

This report is theoretical research starting with searching literature in the library associated with “digital and open bank”. After selecting the essential articles, data the work is done according to the capacity of realization of a mobile bank based on API framework and reliable innovative technologies. The result can be helpful in Kazakhstan for investment and development of the country.

At the moment Kazakhstan has already experience of implementation, becoming the first electronic public framework launched in Central Asia (Kaulanova A., 2017). It is one the initial public system is deployed by API in keeping with Electronic Government as a Service (EgaaS). This has enabled to process just over 40 million electronic requests annually and the number registered users gained on 6 million in 2017 (Egov.kz, 2017). According to the Global UN’s e-Government Knowledgebase (2018), Kazakhstan takes the 39th position of 193 countries.

Going to the bank sector, the situation is slightly different. It is by looking at the information provided by Forbes.kz, the 10 largest commercial banks of Kazakhstan have a stable position (Vorotilov, A. and Aulbekova, A., 2018). There are Halyk Bank JSC, Kaspi Bank JSC, Housing Construction Saving Bank of Kazakhstan JSC, Tsesnabank JSC, SB Sberbank of Russia JSC (Hereinafter — Sberbank), Bank CenterCredit JSC, ForteBank JSC, SB Home Credit Bank JSC, Altyn Bank JSC and ATF Bank JSC (ibid). Most of these banks have own internet version of banking., except Tsesnabank acquired by First Heartland Bank JSC hasn’t mobile and web bank, the online banking work is in progress (First Heartland Bank, 2019).

For instance, the largest bank of Kazakhstan, Halyk Bank after merging with Kazkommertbank that holds 40% market share has myHalyk integrated with Homebank, which the previous owner is Kazkommertbank (Foy, H., 2017). MyHalyk is able to show user’s loans, payment cards and provides money transfer between accounts and others, payment services, account statement as well as currency conversation between Tenge and major currencies (MyHalyk).

However, Kaspi Bank, ForteBank and SberBank provide to society one of the attractive online bank services and their main offers are demonstrated in table1 (Kaspi Bank; ForteBank; SberBank).

Table 1 – Comparison of financial services for clients between three banks.

For security and rapid payments Sberbank, as well as ForteBank, have launched online purchase by ApplePay (Sberbank; ForteBank). At the same time, Kaspi Bank offers to clients instalment purchase of a large number of goods without any extra cost and commission among partner stores of the bank (Kaspi Bank).

Unfortunately, none of the financial institutions of Kazakhstan hasn’t launched the Open API platform allowing to establish interaction between applications for third party companies. This issue provides opportunities for launching digital and mobile bank on the territory of Kazakhstan.

Requirements and opportunities for implementation of a mobile bank

In the previous chapters, the advantages of Starling Bank, as well as the situation of web and mobile banking in Kazakhstan, are discussed. The customer policies of most commercial banks have attractive conditions for clients.

Going to requirements that newly created commercial bank meets to be licensed, the financial regulations are reviewed. According to “On banks and bank activities” Act of the Republic of Kazakhstan, all licensed banks providing financial services are a mandatory member of the insurance system (KDIF, 2019). Due to the fact, the client deposit operated into account is recovered by Kazakhstan Deposit Insurance Fund any terms and conditions (ibid).

Moreover, considering establishing regulatory and calculation methodology for prudential regulation and other mandatory to the observance of the norms and limit of bank capital on given data and Rules of calculation and limits of open foreign exchange position was approved by a Decision of the Board of the National Bank of the Republic of Kazakhstan dated by 13 September 2017 (NBK, 2017). In the document is posted that the minimum- net worth for commercial bank is required to 10 billion KZT(ibid).

Secondly, the following coefficients illustrated in table 2 are entered for determining the capital adequacy of the bank:

Table 2 – The value of capital adequacy ratio (NBK, 2017)

NBK claims that assets, contingent and unforeseen liabilities weighted by risk ratio and introduced in the k1, k1-2, k2 coefficients are formed according to International Financial Reporting Standard (FRS) (NBK, 2017). Besides, the Board’s Decision consists of supplementary and vital requirements for commercial banks such as capital adequacy ratio based on conversation buffer and a mandatory buffer which are not included in the report (ibid).

Another point that should be mentioned, related to human resources of professional IT staff which possible maintains and develops a digital financial product with using last innovative technologies. Kireyeva, A. A., Mussabalina, D. S. and Tolysbaev (2018) believe that in general the IT development of Kazakhstan has acceptable performances where Almaty and Astana play a significant role. The main reasons are educational power of contemporary education institutions as Nazarbayev University works at the same level as western universities or International IT-University collaborated with University Carnegie — Mellon (ibid). In addition, Kazakh-British Technical University trains students in different academic programs who regularly participate in the Association for Computing Machinery – International Collegiate Programming Contest (ACM ICPC) World Championship (KBTU, 2019). As well as KBTU is able to prepare high-level educated students within a double diploma with the London School of Economics for the financial sector (QS Top Universities, 2019). It is an excellent performance of quality education accredited by institution namely IMarEST and Computer Accreditation Commission of ABET and cooperation with British universities (ibid).

Thirdly, in a place where the event of the international specialized exhibition EXPO-2017 was located, the government organized the Astana startup Hub for establishing an innovative project and IT ecosystem (Astana Hub). At the moment, 189 startups, 2034 participants and 60 investors have registered in Astana Hub, the Framework is planning to attract 67 billion KZT as an investment by 2022 (ibid). One of the benefits for launching IT-products within Hub is Law of the preferential tax regime for Astana Hub participants signed by President of the Republic of Kazakhstan (Astana Hub). The document envisages the incentives on a corporate tax income, on individual income tax, on value-added tax, on profit including non-resident and dividends (ibid).

Conclusion

The aim of the essay is to demonstrate the capabilities of the launching digital and mobile bank as Starling Bank uses the innovate approach as an Open API platform (Starling Bank). It was outlined an absence of implementation web bank based on Open API system in Kazakhstan and market situation of domestic high-street banks licensed by National Bank of Kazakhstan which provide financial services. Its services were compared in detail. On the other hand, it was underlined the path where possible to recruit graduated students from Nazarbayev University, International IT-University, (Kireyeva, A. A., et. al., 2018) and Kazak-British Technical University as well- educated engineers to maintain new technologies of the project and professionals in finance and management for the regulation business process (QS Top Universities., 2019). Moreover, it was able to skate the various types of financial preferences of registered residents in Astana Hub who launch products as new high-tech startups (Astana Hub).

Reference

Astana Hub. astanahub.com

Computer Fraud & Security, (2017). UK fraud hits new high., 2017(12), p.3. Egov.kz. (2017). The number of e-Government portal users reached 6 million | Electronic government of the Republic of Kazakhstan.http://egov.kz/cms/en/news/6mln_user [Accessed 28 Feb. 2017].

First Heartland Bank. (2019). First Heartland Securities acquired 99.5% of ordinary shares of Tsesnabank JSC. www.fhb.kz/news/first-heartland-securities-acquired-995-of-ordinary- shares-of-tsesnaba.html?lang=en.

ForteBank. (2019). forte.bank

Foy, H. (2017). Kazakh bank merger to snag 40% market share. Financial Times. www.ft.com/content/afeff74f-bc53-36b8- 9f34-cd05f70dd4d2 [Accessed 15 Dec. 2017].

Haslingden, R. (2018). 16 weeks after Open Banking was brought to market. Experian. Decisions & Credit Risk. www.experian.co.uk/blogs/latest-thinking/decisions-and-credit-risk/16- weeks-open-banking-brought-to-market/ [Accessed 8 May 2018].

Kaulanova, A. (2014). The rise of Open Data in Kazakhstan. [Blog] Information and Communications for Development (IC4D). blogs.worldbank.org/ic4d/rise-open-data-kazakhstan [Accessed 12 Aug. 2014].

KBTU. (2019). Faculty of Information Technologies. www.kbtu.kz/en/fas/fit/about.

Kaspi Bank. (2019). kaspi.kz

Kireyeva, A. A., Mussabalina, D. S. and Tolysbaev, B. S. (2018). Assessment and Identification of the Possibility for Creating IT Clusters in Kazakhstan Regions. Ekonomika Regiona, 14(2), pp.463–473.

KDIF. (2019). Deposit insurance system member banks. www.kdif.kz/en/banki-uchastniki-sistemy-br-garantirovaniya-depozitov Monzo. (2019). [online] Available at: monzo.com

MyHalyk. (2019). myhalyk.kz/wb

NBK (2017). Available at nationalbank.kz/?&switch=english

Park, J., An Y. and K. Yeom, (2016). Virtual cloud bank: An architectural approach for intermediating cloud services. Networking and Parallel/Distributed Computing (SNPD), Takamatsu, 2015, pp. 1-6.

QS Top Universities. (2019). Kazakh-British Technical University. www.topuniversities.com/universities/kazakh-british- technical-university/undergrad

Starling Bank. (2019). [online] Available at: www.starlingbank.com. SberBank. (2019). www.sberbank.kz/en/individuals

Thorell, J. and Sjostrand, J., (2017). Through the Eyes of a Manager: A study on the perceived effects of PSD2 and the preparatory work of Swedish bank managers.

United Nations e-Government Knowledgebase (2018). publicadministration.un.org/egovkb/en-us/Data/Country- Information/id/87-Kazakhstan

Uber.com. Developers | Uber. developer.uber.com/docs/riders/ride-requests/tutorials/api/best- practices#the-basics.

Vorotilov, A. and Aulbekova, A. (2018). Рейтинг банков Казахстана — 2018. Forbes Kazakhstan. forbes.kz/leader/reyting_bankov_kazahstana_2018_1532941613

Computer Fraud & Security, (2017). UK fraud hits new high., 2017(12), p.3. Egov.kz. (2017). The number of e-Government portal users reached 6 million | Electronic government of the Republic of Kazakhstan.http://egov.kz/cms/en/news/6mln_user [Accessed 28 Feb. 2017].

First Heartland Bank. (2019). First Heartland Securities acquired 99.5% of ordinary shares of Tsesnabank JSC. www.fhb.kz/news/first-heartland-securities-acquired-995-of-ordinary- shares-of-tsesnaba.html?lang=en.

ForteBank. (2019). forte.bank

Foy, H. (2017). Kazakh bank merger to snag 40% market share. Financial Times. www.ft.com/content/afeff74f-bc53-36b8- 9f34-cd05f70dd4d2 [Accessed 15 Dec. 2017].

Haslingden, R. (2018). 16 weeks after Open Banking was brought to market. Experian. Decisions & Credit Risk. www.experian.co.uk/blogs/latest-thinking/decisions-and-credit-risk/16- weeks-open-banking-brought-to-market/ [Accessed 8 May 2018].

Kaulanova, A. (2014). The rise of Open Data in Kazakhstan. [Blog] Information and Communications for Development (IC4D). blogs.worldbank.org/ic4d/rise-open-data-kazakhstan [Accessed 12 Aug. 2014].

KBTU. (2019). Faculty of Information Technologies. www.kbtu.kz/en/fas/fit/about.

Kaspi Bank. (2019). kaspi.kz

Kireyeva, A. A., Mussabalina, D. S. and Tolysbaev, B. S. (2018). Assessment and Identification of the Possibility for Creating IT Clusters in Kazakhstan Regions. Ekonomika Regiona, 14(2), pp.463–473.

KDIF. (2019). Deposit insurance system member banks. www.kdif.kz/en/banki-uchastniki-sistemy-br-garantirovaniya-depozitov Monzo. (2019). [online] Available at: monzo.com

MyHalyk. (2019). myhalyk.kz/wb

NBK (2017). Available at nationalbank.kz/?&switch=english

Park, J., An Y. and K. Yeom, (2016). Virtual cloud bank: An architectural approach for intermediating cloud services. Networking and Parallel/Distributed Computing (SNPD), Takamatsu, 2015, pp. 1-6.

QS Top Universities. (2019). Kazakh-British Technical University. www.topuniversities.com/universities/kazakh-british- technical-university/undergrad

Starling Bank. (2019). [online] Available at: www.starlingbank.com. SberBank. (2019). www.sberbank.kz/en/individuals

Thorell, J. and Sjostrand, J., (2017). Through the Eyes of a Manager: A study on the perceived effects of PSD2 and the preparatory work of Swedish bank managers.

United Nations e-Government Knowledgebase (2018). publicadministration.un.org/egovkb/en-us/Data/Country- Information/id/87-Kazakhstan

Uber.com. Developers | Uber. developer.uber.com/docs/riders/ride-requests/tutorials/api/best- practices#the-basics.

Vorotilov, A. and Aulbekova, A. (2018). Рейтинг банков Казахстана — 2018. Forbes Kazakhstan. forbes.kz/leader/reyting_bankov_kazahstana_2018_1532941613

DaemonGloom

Looks like there is a problem with rss feed. That post is linked as russian one (https://habr.com/ru/post/441770/) but it should be on /en/ part of the site.

Exosphere

Fixed by moderator. Thank you.